AI-Fueled Finance Fraud Is Up 1,210%: How CFOs Are Protecting AP and AR Teams in 2026

AI-driven fraud attacks on finance teams rose 1,210% in 2025. Deepfake BEC attacks on AP are now the #1 new threat vector. Here is the specific protection playbook CFOs are deploying right now.

- The Stat: AI-driven fraud attacks on finance organizations rose 1,210% in 2025, with combined losses estimated at $1 billion. Source: CFO Dive, citing Pindrop research, 2026.

- Top Attack Vector: Deepfake audio and video BEC attacks targeting AP teams for payment changes and wire transfers. The AI voice is trained on publicly available audio of the impersonated executive.

- Secondary Vectors: AI-generated phishing emails indistinguishable from real vendor communications; synthetic identity fraud in AR; AI-assisted invoice fraud using near-identical vendor names.

- The Defense: Five-layer protection model combining process controls, AI pattern detection, dual-approval gates, vendor portal verification, and staff training on deepfake recognition.

- AI as Defense: The same AI capability that enables fraud also detects it. Pattern recognition across AP and AR transaction data surfaces anomalies invisible to human reviewers in high-volume environments.

Finance fraud has always been a CFO concern. What changed in 2025 was the technology available to attackers. AI voice cloning, AI-generated email text, AI-assisted document forgery, and deepfake video have lowered the technical barrier to financial fraud to near zero. Anyone with a laptop and a free AI tool can produce a convincing CFO voice instructing an AP team member to wire $200,000 immediately.

CFO Dive reported a 1,210% increase in AI-driven fraud attacks in 2025, with $1 billion in combined losses. PYMNTS documented the trend as "Fraud Is Knocking Louder on the CFO's Door." The primary target is not the IT department. It is the finance function, specifically AP and AR teams who process payments and manage banking relationships.

The good news is that AI defends as effectively as it attacks. The finance teams that have avoided major fraud incidents in 2026 have deployed the same AI pattern recognition capability against their own transaction data that fraudsters are deploying against them. This article covers both the threat landscape and the specific countermeasures that work.

What Are the Five Primary AI-Driven Fraud Vectors Targeting Finance Teams in 2026?

"Fraud is no longer distinguishable from legitimate communication by appearance or sound alone. The only reliable defense is process controls that do not depend on human judgment in the moment." — CFO, mid-market manufacturing company, 2026

What Is the Five-Layer Finance Fraud Protection Framework?

Layer 1: Vendor bank account verification via secure portal only. Bank account additions and changes must be submitted through a vendor self-service portal that requires multi-factor authentication and is completely separate from email. No bank account change request received via email, phone, or any other channel is processed without portal resubmission. This single control eliminates the primary BEC payment redirect vector.

Layer 2: AI pattern detection across AP and AR transaction data. AI monitors all payment behavior for anomalies: amounts just below approval thresholds, new vendor with first payment within 48 hours of creation, payment to a vendor whose name closely matches an existing vendor, payment frequency pattern changes for established vendors, AR credits applied to recently opened accounts.

Layer 3: Dual-approval for all first-time and high-value payments. First payment to any vendor requires two approvers. All payments above the materiality threshold require two approvers, with at least one approval coming from a finance manager, not a processor. Approval requests received outside of business hours are held for next-business-day review, not processed immediately.

Layer 4: Call-back verification using pre-registered numbers only. Any payment change, urgency claim, or bank detail update received via any channel triggers a call-back verification using only the phone number registered in the vendor master, not the number provided in the communication. The call-back is initiated by AP, not returned to the caller.

Layer 5: Deepfake recognition training and escalation protocol. All AP and AR staff complete deepfake recognition training annually. The protocol for any communication that requests an urgent payment outside normal workflow is: stop, escalate to the finance manager, and initiate the call-back verification process. Time pressure in a fraud request is always a red flag.

How Does AI Pattern Detection Catch Fraud That Humans Miss?

The same AI capability that enables finance fraud also detects it. AI pattern recognition operates continuously across the full volume of transaction data, identifying statistical anomalies that would be invisible in manual review of individual transactions.

| Fraud Pattern | Human Detection Rate | AI Detection Rate |

|---|---|---|

| Duplicate invoice (same vendor, slight amount variation) | ~40% caught on review | 99%+ at ingestion |

| Payment just below approval threshold | ~15% flagged | 100% flagged by pattern analysis |

| Near-identical vendor name (1 character different) | ~25% caught | 100% flagged on vendor creation |

| New vendor, first payment within 48 hours | ~50% reviewed | 100% flagged and held |

| Bank account change followed immediately by payment | ~30% caught | 100% flagged with correlation alert |

| AR credit to recently opened account | ~20% reviewed | 100% flagged with account age alert |

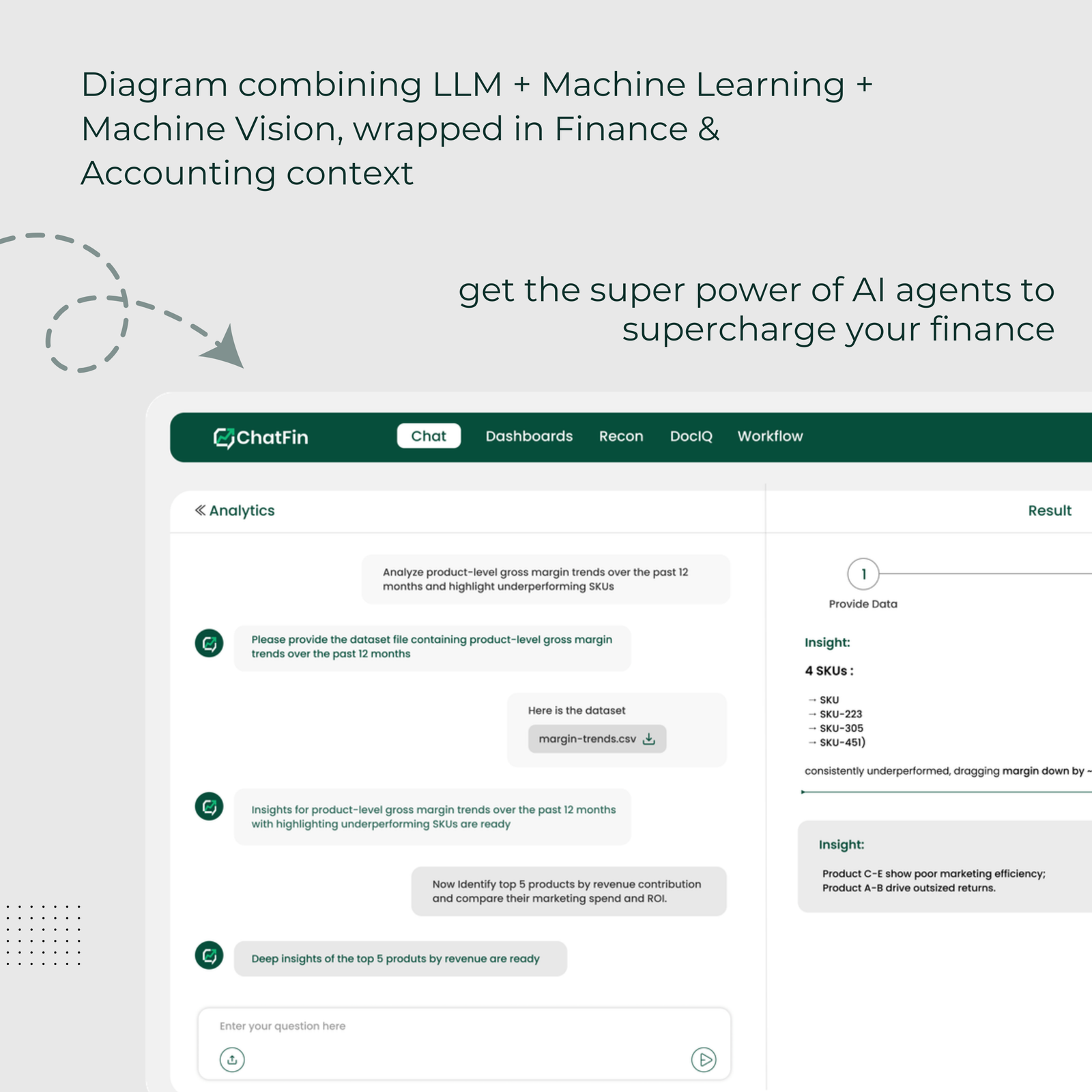

What Are the Specific AI Controls ChatFin Deploys for Finance Fraud Detection?

ChatFin's Pattern Recognition Agent monitors AP and AR transaction data in real time for behavioral anomalies. Every alert includes the specific transaction, the anomaly pattern detected, the risk classification, and a recommended action for the finance team.

Frequently Asked Questions

How much has AI-fueled finance fraud increased?

What is a deepfake BEC attack on accounts payable?

How can CFOs protect AP teams from AI-driven fraud?

Does AI help detect finance fraud as well as enable it?

How does ChatFin help detect finance fraud?

The Same AI That Enables Fraud Also Stops It. The Question Is Who Deploys It First.

The 1,210% increase in AI-driven finance fraud is not a reason to slow down AI adoption in finance operations. It is a reason to deploy AI defensively as urgently as you deploy it offensively. Every AP and AR function that processes transactions manually at volume is operating with significant blind spots that fraudsters are now systematically targeting.

The five-layer protection framework is not expensive or complex to implement. The process controls, vendor portal, and dual-approval requirements require policy changes, not technology. The AI pattern detection layer requires a platform that connects to your transaction data, which is where ChatFin fits. The training requirement is a 2-hour annual session.

Finance fraud in 2026 is an arms race. The finance teams that win it are the ones that deploy AI detection as fast as fraudsters deploy AI attacks.