AI for Audit Readiness: How Finance Teams Are Preparing for External Audits with AI Agents in 2026

PCAOB delivered major guidance on AI in auditing. COSO released AI governance standards for generative AI in finance. Big 4 firms are deploying AI across audit workflows. Here is how finance teams are using AI agents to prepare for external audits — and why continuous audit readiness is replacing the annual scramble.

- PCAOB and COSO both released major AI guidance for auditing in early 2026 — setting new documentation and governance standards for AI use in finance.

- Big 4 firms are deploying AI tools across audit workflows, meaning auditors will arrive with AI that can analyze your financial data faster than any manual review.

- Continuous audit readiness — maintaining audit evidence year-round rather than preparing it annually — is now achievable with AI agents.

- Four AI capabilities most reduce audit preparation time: automated reconciliation, PBC list auto-population, anomaly pre-detection, and GL audit trail generation.

- Finance teams using AI agents for audit readiness report 50-60% reduction in audit preparation hours and fewer auditor findings in the first year.

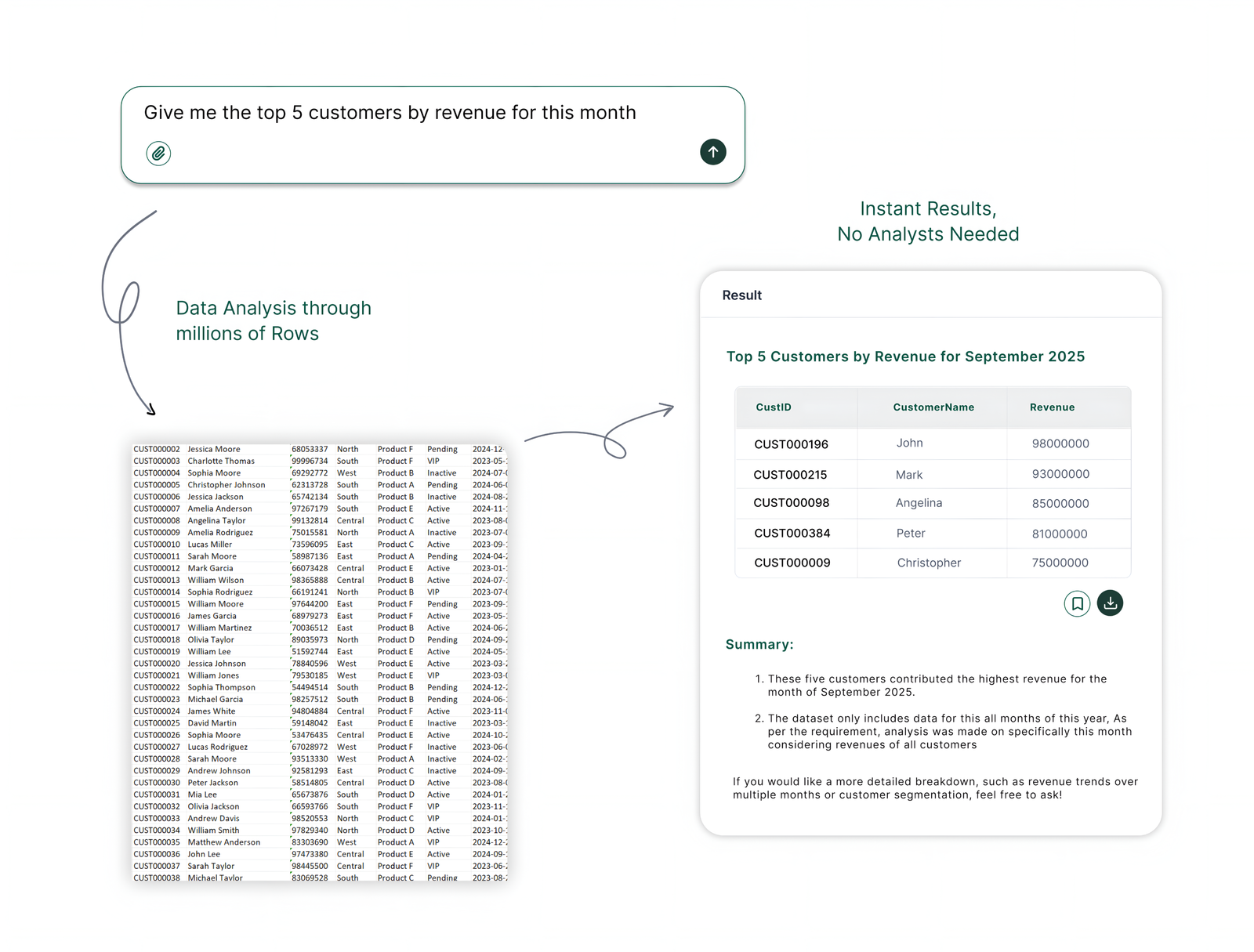

The external audit has traditionally been the most disruptive period in the finance calendar. For six to ten weeks, the finance team divides its time between day-to-day operations and responding to an ever-expanding PBC (provided by client) list from the audit team. Controllers estimate that their teams spend 200-400 hours per audit cycle on preparation and response work that could, in principle, be prepared continuously throughout the year.

Two developments in 2026 are changing this calculation. First, PCAOB and COSO both released major AI governance frameworks specifically addressing AI in audit and finance. Second, auditors themselves are arriving with AI tools that can analyze transaction data faster than human review — meaning finance teams that have not already maintained clean, documented financials will face more questions, not fewer.

The response from leading finance teams is a shift to continuous audit readiness: using AI agents to maintain audit documentation, reconciliations, and evidence packages throughout the year, so the audit PBC list becomes a retrieval exercise rather than an emergency research project.

What Did PCAOB and COSO Release About AI in Auditing in 2026?

The regulatory activity around AI and auditing in 2026 has been significant. Two major publications define the current governance landscape:

- PCAOB speech on AI and audit quality: The Public Company Accounting Oversight Board delivered "AI and the Pursuit of Audit Quality: A Regulatory Perspective" in 2026. Key requirements: auditors using AI must document AI tool outputs as part of their audit evidence; professional skepticism applies to AI-generated conclusions; and AI-assisted procedures must meet the same evidentiary standards as manual procedures. This matters for finance teams because it means auditors using AI will generate more documented findings — requiring stronger supporting evidence from the company's finance team.

- COSO AI governance guidance: In February 2026, COSO published audit-ready governance guidance for generative AI. The Journal of Accountancy covered it as a landmark standard for finance AI governance. Key requirements: organizations using generative AI in financial reporting must document AI model inputs and outputs; maintain complete audit trails of AI agent actions; establish human review checkpoints for AI-generated financial information; and disclose AI use in financial reporting processes to auditors.

"Auditors are arriving with AI that can analyze 100% of your transactions in hours. Finance teams that prepare for audit readiness year-round — rather than scrambling in Q1 — will have dramatically fewer findings and faster audits."

Journal of Accountancy, "How AI Is Transforming the Audit — and What It Means for CPAs," February 2026How Are Big 4 Firms Deploying AI in Audit Workflows?

The Big 4 AI deployments documented in 2026 include audit-specific applications that directly affect how external audits are conducted:

- EY: Deployed AI agents capable of reviewing 100% of transactions rather than audit samples — changing the audit from statistical sampling to full-population analysis. Finance teams accustomed to audit samples now face AI that examines every transaction.

- Deloitte: Zora AI handles document review and financial statement analysis, flagging anomalies and inconsistencies for auditor investigation. Finance teams will need stronger documentation for any items that Deloitte's AI flags as unusual.

- PwC: GL.ai performs journal entry and general ledger review, specifically targeting manual journal entries — one of the highest-risk areas in financial statement audits. Finance teams with high volumes of manual JEs should expect more scrutiny.

- KPMG: $2B AI investment includes audit analytics tools that compare a company's financial ratios and trends against industry benchmarks automatically. Finance teams with unusual ratios — even legitimate ones — will need to prepare explanations proactively.

What Does AI-Driven Audit Readiness Look Like in Practice?

| Audit Activity | Traditional Approach | AI-Driven Approach | Time Saved |

|---|---|---|---|

| PBC list population | Manual document search + compilation, 40-80 hours | AI auto-populates from ERP transaction history | 60-75% |

| Account reconciliations | Manual monthly reconciliation, reviewed annually at audit | Continuous AI reconciliation with documented variances | 50-65% |

| Variance explanations | Finance team writes explanations under audit pressure | AI generates variance commentary throughout the year | 70-80% |

| Anomaly identification | Auditors surface issues during fieldwork | AI pre-identifies and resolves issues before auditors arrive | Fewer findings |

| Audit evidence packaging | Manual document assembly per auditor request | AI retrieves and packages evidence from indexed documentation | 55-70% |

What Are the Four AI Capabilities That Most Reduce Audit Preparation Time?

- Automated reconciliation with audit trails: AI agents run reconciliations continuously — bank reconciliations, intercompany reconciliations, sub-ledger to GL reconciliations — and document every variance with a timestamped explanation. When auditors request reconciliation documentation, the AI retrieves it instantly rather than requiring finance staff to reconstruct months of activity.

- PBC list auto-population: AI agents with ERP access can respond to auditor PBC requests by querying transaction data, contracts, and supporting documentation directly. A PBC request that would take a finance analyst two days to respond to manually can be fulfilled in hours with AI retrieval.

- Anomaly pre-detection: Running the same pattern analysis that auditors will run — before auditors arrive — allows finance teams to identify and resolve issues proactively. Finance teams that surface and explain unusual transactions before the audit fieldwork begins consistently report fewer audit findings and shorter audit cycles.

- GL audit trail generation: AI agents maintain machine-readable audit trails for all journal entries, including the source, approver, business purpose, and supporting documentation for each entry. This is particularly important as auditors deploy AI tools that analyze 100% of JEs rather than sampling.

COSO AI Governance Requirements for Finance Teams Using AI

COSO's February 2026 guidance requires organizations using generative AI in financial reporting to meet four specific requirements:

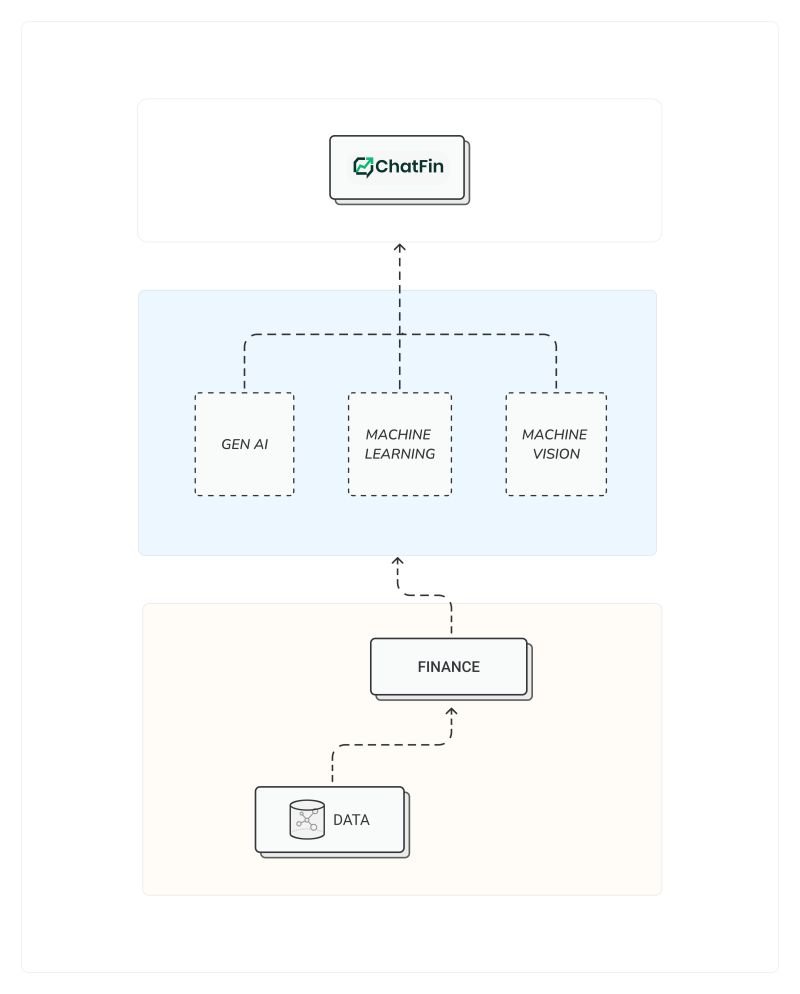

1. Document AI inputs and outputs: Every AI-generated financial analysis, reconciliation, or report must document the inputs the AI used and the outputs it produced. ChatFin generates this documentation automatically as part of each agent action.

2. Maintain AI audit trails: Complete logs of AI agent actions — what the agent queried, what it produced, when, and with what confidence — must be available for auditor review. ChatFin's audit trail meets COSO 2026 requirements.

3. Human review checkpoints: AI-generated financial information must pass through documented human review before inclusion in financial statements. ChatFin's workflow includes configurable human review gates at each reporting stage.

4. Auditor disclosure: Finance teams must disclose AI use in financial reporting processes to external auditors. ChatFin provides a standard AI use disclosure template aligned with COSO guidance.

How Should Finance Teams Prioritize AI Audit Readiness Investments?

Not all audit preparation activities benefit equally from AI. The highest-ROI applications to prioritize are:

- Journal entry analysis: Given that PwC and KPMG have deployed AI specifically targeting journal entries, finance teams should prioritize AI monitoring of manual JEs — ensuring all entries have documented business purposes and supporting evidence.

- Account reconciliation automation: Automating reconciliations produces benefits year-round, not just during audit. Finance teams that implement continuous reconciliation report not only faster audits but also faster monthly closes.

- Revenue recognition documentation: Revenue recognition under ASC 606 is consistently the highest-risk audit area for companies with complex contracts. AI agents that maintain contract modification logs, variable consideration calculations, and performance obligation documentation dramatically reduce audit risk in this area.

- Related-party transaction documentation: Related-party transactions are scrutinized closely in every external audit. AI agents can maintain contemporaneous documentation for all related-party transactions — including business purpose, pricing support, and approval chains — throughout the year.

Frequently Asked Questions About AI Audit Readiness

What is AI audit readiness in finance?

What did PCAOB say about AI in audits in 2026?

What did COSO release about AI governance for auditing in 2026?

How do AI agents reduce audit preparation time?

Does using AI in finance create additional audit risk?

The Bottom Line on AI Audit Readiness

The external audit is no longer a once-a-year event that the finance team prepares for in isolation. Big 4 firms are arriving with AI that analyzes 100% of transactions, PCAOB and COSO have published new AI governance requirements, and finance teams that prepare continuously — rather than annually — have measurably better audit outcomes.

The practical investment case is strong. Finance teams that implement AI audit readiness report 50-60% reduction in audit preparation hours — time that translates directly into lower audit fees and reduced internal labor costs. They also report fewer audit findings and faster fieldwork cycles, because auditors spend less time surfacing issues that the finance team has already identified and documented.

ChatFin's Finance AI Super Agent is built to maintain continuous audit readiness across your full financial close, reconciliation, and reporting stack — generating COSO-compliant audit trails automatically and responding to auditor PBC requests from structured ERP data.

See Audit Readiness in Action